1. What is the Radiation-Hardened Electronics Market Overview – definition, scope, and significance?

The Radiation-Hardened Electronics (RHE) market comprises electronic components and systems engineered to operate reliably in high‑radiation environments such as space, nuclear facilities, and defense applications. Scope includes power management, mixed‑signal devices, memory, and processors produced through design‑level or process‑level hardening techniques. Its significance lies in enabling mission‑critical operations where failure can result in catastrophic loss of data, equipment, or human safety, making it a cornerstone for aerospace, defense, and nuclear sectors.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Radiation-Hardened Electronics Market?

Key drivers include rising satellite launches, increased defense spending on resilient systems, and the need for reliable electronics in nuclear power plants. Restraints stem from high development costs and stringent certification requirements. Challenges involve limited supplier base and long lead times for qualified parts. Opportunities arise from emerging small‑satellite constellations, growing interest in deep‑space exploration, and advancements in radiation‑hardening by design that can reduce costs while maintaining performance.

3. What growth trends are currently influencing the Radiation-Hardened Electronics Market?

Current trends feature a shift toward system‑on‑chip (SoC) architectures that integrate multiple hardened functions, the adoption of advanced process nodes for better power efficiency, and a rise in commercial‑off‑the‑shelf (COTS) components enhanced through hardening by design. Additionally, government programs promoting resilient infrastructure are accelerating demand, while collaborations between semiconductor firms and aerospace agencies foster rapid technology transfer.

4. How has COVID‑19 impacted the Radiation-Hardened Electronics Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in supply chains and delayed satellite program schedules, leading to a short‑term dip in orders. However, because RHE products are tied to long‑term defense and space contracts, the market rebounded quickly. Post‑COVID, demand accelerated as governments prioritized strategic resilience, and the recovery trajectory is now strong, with growth projected to outpace many other semiconductor segments.

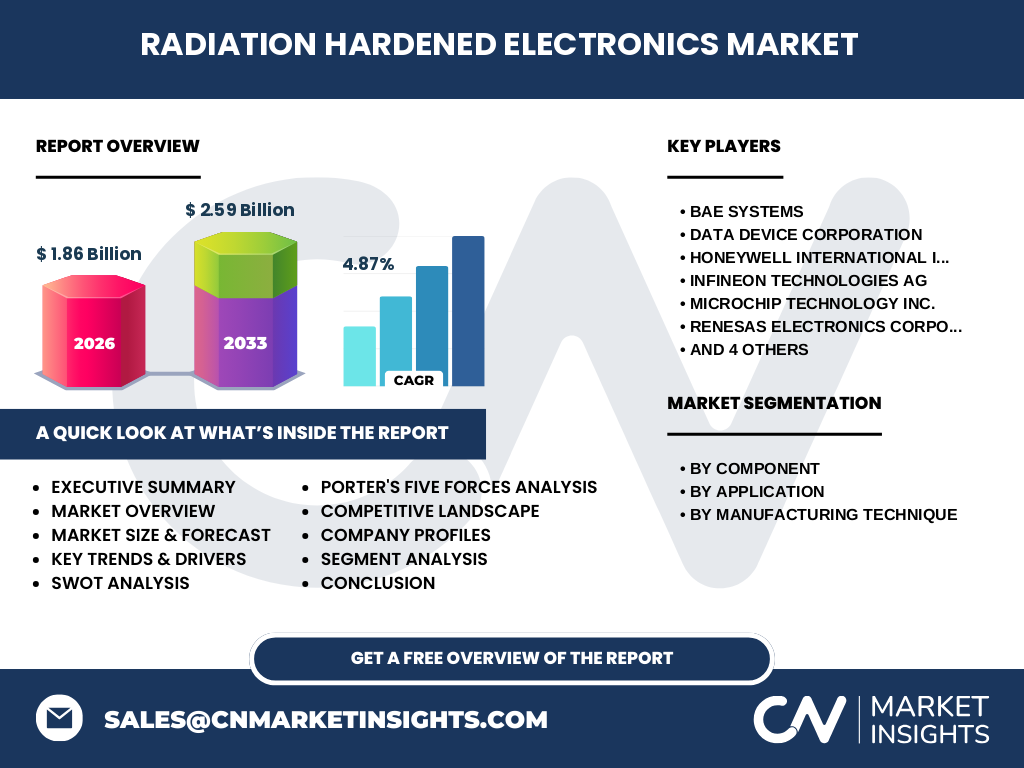

5. Who are the major competitors and what is the competitive landscape of the Radiation-Hardened Electronics Market?

Prominent players include BAE Systems, Data Device Corporation, Honeywell International, Infineon Technologies, Microchip Technology, Renesas Electronics, STMicroelectronics, Texas Instruments, VORAGO Technologies, and Xilinx (AMD). The landscape is characterized by high entry barriers, a few dominant firms with deep heritage in radiation testing, and recent consolidation as larger companies acquire niche specialists to broaden their hardened portfolio and improve economies of scale.

6. What are the key findings highlighted in the Executive Summary of the Radiation-Hardened Electronics Market?

The market is valued at $1.86 billion in 2026 and is projected to reach $2.59 billion by 2033, reflecting a CAGR of 4.87 %. Growth is fueled by expanding space initiatives, defense modernization, and nuclear safety requirements. Design‑level hardening is gaining traction due to cost advantages, while regional demand remains strongest in North America and Europe. Competitive pressure is intensifying as firms leverage advanced processes and strategic partnerships.

7. What are the market forecasts for the Radiation-Hardened Electronics Market from 2025 to 2032?

Based on the provided CAGR of 4.87 %, the market is expected to continue its steady rise, moving from the 2026 baseline of $1.86 billion toward the 2033 forecast of $2.59 billion. Annual growth will be driven by new satellite constellations, defense procurement cycles, and incremental adoption of hardened components in emerging nuclear reactor designs.

8. How is the Radiation-Hardened Electronics Market sized and shared by component, application, and manufacturing technique segments?

By component, the market is split among power management components, analog & digital mixed‑signal devices, memory, and controllers & processors. Application segmentation covers aerospace & defense, nuclear power plants, and space. Manufacturing techniques are divided between radiation hardening by design and radiation hardening by process. While exact monetary shares are not disclosed, each segment reflects the diversified needs of mission‑critical environments, with aerospace & defense typically commanding the largest portion.

9. What is the geographic distribution of the global Radiation-Hardened Electronics Market?

The market exhibits strong presence in North America, Europe, and the Asia‑Pacific region. North America leads due to extensive defense programs and NASA initiatives, Europe follows with robust aerospace activities, and Asia‑Pacific shows rapid growth driven by emerging satellite operators and increasing nuclear energy projects. The global footprint underscores a balanced yet regionally nuanced demand pattern.

10. What are the detailed regional performances in the Radiation-Hardened Electronics Market?

In North America, government contracts for missile systems and space missions drive the bulk of sales. Europe’s market is bolstered by ESA projects and defense collaborations among EU nations. Asia‑Pacific’s growth is propelled by commercial satellite constellations, government‑led nuclear expansions, and rising defense budgets. Each region benefits from local expertise, regulatory frameworks, and strategic investments that shape market dynamics.

11. Which companies lead the Radiation-Hardened Electronics Market and what are their key strategies?

Leaders such as BAE Systems focus on integrated defense solutions, while Data Device Corporation emphasizes high‑reliability memory. Honeywell leverages its aerospace heritage, Infineon invests in advanced process hardening, and Microchip expands its portfolio through acquisitions. Renesas and STMicroelectronics target mixed‑signal devices, Texas Instruments emphasizes analog performance, VORAGO develops silicon‑on‑insulator (SOI) technologies, and Xilinx (AMD) provides radiation‑hardened FPGAs. Common strategies include R&D investment, strategic partnerships, and portfolio diversification.

12. How does Porter’s Five Forces analysis apply to the Radiation-Hardened Electronics Market?

Threat of new entrants is low due to high certification costs and specialized expertise. Bargaining power of suppliers is moderate; few foundries offer qualified radiation‑hardening processes. Buyer power is relatively high because defense and aerospace customers demand stringent specifications and competitive pricing. The threat of substitutes is limited, as few alternatives match the reliability required in high‑radiation settings. Competitive rivalry is intense, driven by innovation cycles and the need for long‑term support contracts.

13. What are the SWOT strengths, weaknesses, opportunities, and threats for the Radiation-Hardened Electronics Market?

Strengths include proven reliability, critical mission relevance, and a loyal customer base. Weaknesses involve high cost structures and long development timelines. Opportunities arise from miniaturized satellite platforms, next‑generation nuclear reactors, and emerging hardening‑by‑design methodologies. Threats consist of supply chain disruptions, rapid technology obsolescence, and potential geopolitical restrictions affecting cross‑border component sourcing.

14. How does the value chain of the Radiation-Hardened Electronics Market operate?

The value chain begins with raw material suppliers (high‑purity silicon, radiation‑hardening chemicals), proceeds to specialized foundries that apply hardening by process, followed by design houses that implement hardening by design. Subsequent stages include testing and qualification labs, system integrators, and final end‑users in aerospace, defense, and nuclear sectors. Each step adds critical validation to ensure compliance with stringent radiation tolerance standards.

15. What key investment insights can be drawn from the Radiation-Hardened Electronics Market?

Investors should focus on companies with strong R&D pipelines in hardening‑by‑design, as this approach lowers cost while maintaining performance. Strategic acquisitions of niche memory or SOI specialists can provide quick market entry. Long‑term contracts with government agencies offer revenue stability, making firms with a diversified defense and space customer base attractive for sustained growth.

16. What are the primary conclusions and takeaways from the Radiation-Hardened Electronics Market analysis?

The market is on a steady growth path, underpinned by critical defense and space missions. A 4.87 % CAGR to $2.59 billion by 2033 reflects resilience and expanding demand. Technical innovation, especially in design‑level hardening, will dictate competitive advantage. Geographic diversification and strategic partnerships remain essential for capturing emerging opportunities while mitigating supply‑chain risks.

17. What research methodology was employed to develop this Radiation-Hardened Electronics Market report?

Primary research included interviews with industry experts, major OEMs, and end‑users across aerospace, defense, and nuclear sectors. Secondary sources comprised company filings, government procurement databases, and reputable market intelligence reports. Data triangulation ensured consistency, while forecasting employed the provided CAGR of 4.87 % to project future market size.

18. What is the scope of this research and its limitations?

The study covers global market sizing, segmentation by component, application, and manufacturing technique, as well as regional analysis for major geographies. It excludes detailed financial breakdowns beyond the provided figures and does not quantify individual segment shares. The analysis focuses on publicly available information up to 2026 and forecasts through 2033, acknowledging that unforeseen regulatory or geopolitical events could influence outcomes.

19. Which key companies have recent developments in the Radiation-Hardened Electronics Market?

Recent announcements include BAE Systems securing a multi‑year defense contract for hardened processors, Data Device Corporation launching a new radiation‑tolerant memory line, Honeywell unveiling upgraded power‑management modules for satellite platforms, Infineon introducing a 28 nm hardening‑by‑process technology, and VORAGO unveiling an SOI‑based FPGA targeting deep‑space missions. Xilinx (AMD) expanded its hardened FPGA portfolio with a focus on AI‑ready space applications, while Texas Instruments released a mixed‑signal device optimized for radiation environments.